Profit and loss solutions for SSC CGL Tier 2 Set 8

Profit and loss questions with solutions for SSC CGL Tier 2 Set explains how to solve the 10 questions conceptually and quickly in time.

If you have not taken the test yet, take the test first at,

SSC CGL Tier II level Question Set 8, Profit and loss 1.

Profit and loss questions with solutions for SSC CGL Tier 2 set 8 - Answering time was 12 mins

Problem 1.

A dealer purchased a microwave oven for Rs.7660. After giving a discount of 12% on its marked price, he still gained 10%. The marked price was,

- Rs.9755

- Rs.8426

- Rs.8246

- Rs.9575

Solution 1 - Problem analysis

The percentage of discount is on the marked price, say, $M$ which is to be found out, whereas the profit percentage of 10% is on the given cost price of Rs.7660. While adding the profit to the cost price we get the sale price, the same sale price we would get by subtracting the discount from the marked price.

Using percentage application concept for profit and loss we can say,

$\text{Sale price}=M-\text{12% of }M=0.88M$

Similarly adding profit percentage to the cost price we would get,

$\text{Sale price}=7660+\text{10% of }7660=1.1\text{ of }7660$.

We have delayed the multiplication of 7660 by 1.1 as we knew 11 will be canceled out later. This is application of delayed evaluation technique which is a component of efficient simplification.

Solution 1 - Problem solving execution

We have arrived at the sale price from marked price by reducing it by discount, and also from the cost price by increasing it by profit. Now we only have to equate the two sale prices,

$0.88M=1.1\times{7660}$,

Or, $M=\displaystyle\frac{76600}{8}$, we have eliminated all decimals by multiplying by 10s multiples and canceled out 11,

Or, $M=9575$, dividing directly by 8.

Answer: Option d: Rs.9575.

Key concepts used: Basic profit and loss concepts -- Rich profit and loss concepts -- marked price concept -- discount concept -- percentage application concept for profit and loss, you need to apply the percentage profit on cost price and percentage discount on marked price -- efficient simplification, the presence of the factor of 11 was detected and utilized -- delayed evaluation technique -- decimal elimination technique.

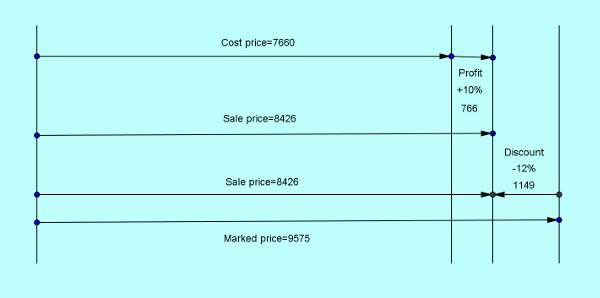

Explanation based on Graphical representation

The following is the graphical representation of the problem,

Reduction of marked price by 12% results in the value of Sale price as $0.88M$ which converges with the Sale price arrived at by addition of 10% profit to Cost price, that is, $1.1\text{ of }7660$.

Note. One can solve the problem wholly mentally using the rich profit and loss concepts and the technique of delayed evaluation. Division of 76600 by 8 is simple.

Problem 2.

If a man were to sell a chair for Rs.720, he would lose 25%. For gaining 25%, he has to sell it for,

- Rs.960

- Rs.1000

- Rs.1200

- Rs.900

Solution 2 - Problem analysis and solving

Here also by the anchor value of percentage concept where anchor is the cost, though the value the cost price on which profit and loss percentages are to be applied, is not given, from the loss percentage of 25% and sale price of Rs.720 of the first transaction we can conclude,

$\text{Sale price }=720=\text{Cost price }-\text{25% of Cost price}$,

Or, $\text{Cost price }=\frac{4}{3}\times{720}$.

If target profit is 25%, the target sale price would have to be,

$\text{Target sale price }=1.25\text{ of Cost price}$

$=\frac{5}{4}\times{\frac{4}{3}}\times{720}$

$=1200$

Again we have used delayed evaluation technique to cancel out factors at the last stage and carry out a simplified calculation just once.

Answer: Option c : Rs.1200.

Key concepts used: Basic profit and loss concepts -- anchor value of percentage concept, for profit or loss the percentage is to be usually applied on the anchor value of the cost price -- delayed evaluation technique.

Problem 3.

Purchasing a motorcycle from Surya, Naveen spent Rs.1680 on it for repair and sold it to Pintu for Rs.35910 at a profit of 12.5%. If Surya sold the motorcycle to Naveen at a loss of 28%, the purchase cost of the motorcycle for Surya is,

- Rs.35000

- Rs.38000

- Rs.40000

- Rs.42000

Solution 3 - Problem analysis and solving

Usually in Profit and loss problems two events happen, but in this problem we see four events. To deal with the apparent confusion we must first clearly plot out the events in time sequence,

1. First: Surya purchased a motorcycle at cost $C$ which is to be found out.

2. Second: Surya sold the motorcycle to Naveen at a loss of 28%. So the cost price to Naveen was, $0.72C$, less 28% of $C$. This was the sale price of Surya.

3. Third: Naveen spent an additional amount of Rs.1680 for repair making its effective cost to him as, $0.72C + 1680$.

4. Fourth: Naveen sold the motorcycle thus repaired to Pintu at a profit of 12.5% which is one-eighth more than his cost price. In other words,

$\text{Naveen's sale price }=\frac{9}{8}\text{ of }(0.72C +1680)=35910$.

Solution 3 - Problem solving execution final stage

So,

$0.72C +1680=\frac{8}{9}\times{35910}=8\times{3990}=31920$,

Or, $0.72C=30240$,

Or, $C=\displaystyle\frac{3024000}{72}=42000$.

Answer: d: Rs.42000.

Key concepts used: Sequencing of events -- basic profit and loss concepts -- percentage conversion techniques -- efficient simplification.

Note: Without sequencing of the events one after the other, it won't have been possible to get a clear idea of the costs and prices involved. Additionally in profit and loss problems as a part of efficient simplification, we convert percentages in two ways, either as a decimal or as a fraction as the need may be. This is percentage conversion techniques.

The most used percentages and corresponding fractions are useful to remember,

1. $4\text{%}=\frac{1}{25}$

2. $5\text{%}=\frac{1}{20}$

3. $8\text{%}=\frac{2}{25}$

4. $10\text{%}=\frac{1}{10}$

5. $12.5\text{%}=\frac{1}{8}$

6. $20\text{%}=\frac{1}{5}$

7. $25\text{%}=\frac{1}{4}$

8. $30\text{%}=\frac{3}{10}$

9. $40\text{%}=\frac{2}{5}$

10. $50\text{%}=\frac{1}{2}$

11. $60\text{%}=\frac{3}{5}$

12. $75\text{%}=\frac{3}{4}$

13. $80\text{%}=\frac{4}{5}$

14. $90\text{%}=\frac{9}{10}$.

$72\text{%}$ didn't correspond to any convenient fraction and so we have used instead its equivalent decimal form, $0.72$, dividing it by 100.

Problem 4.

Praveen bought a plot of land for Rs.96000 and sold $\frac{2}{5}$th of it at a loss of 6%. If he wanted to make a profit of 10% on the whole transaction by selling the remaining land, the gain % of the remaining land must then be,

- $20\text{%}$

- $20\frac{2}{3}\text{%}$

- $7\text{%}$

- $14\text{%}$

Solution 4 - Problem analysis and solving

Desired profit on whole land transaction is,

$10\text{% of }96000=\frac{1}{10}\times{96000}$

Loss in the first transaction is $6\text{% of }\frac{2}{5}\text{th of }96000=\frac{3}{125}\text{ of }96000$. This has been the shortfall.

So total desired profit is,

$\frac{1}{10}\times{96000}=\text{profit on}\frac{3}{5}\times{96000} - \frac{3}{125}\times{96000}$,

Or, $P\times{\frac{3}{5}}=\frac{1}{10}+\frac{3}{125}$,

Or, $P=\frac{1}{6}+\frac{1}{25}=\frac{31}{150}=\frac{62}{3}\text{%}=20\frac{2}{3}\text{%}$

Answer: Option b: $20\frac{2}{3}\text{%}$.

Key concepts used: Profit and loss basic concepts -- two stage transaction concepts -- complete bypassing of multiplication of factor 96000 because all of the profits and losses are some portion of this whole -- efficient simplification -- percentage conversion techniques -- fraction arithmetic -- percentage concepts.

Problem 5.

A shopkeeper bought two watches at a total cost of Rs.840. He then sold one at a loss of 12% and the other at a profit of 16%. There was no loss or gain in the whole transaction. The cost price of the watch on which the shopkeeper gained was then,

- Rs.390

- Rs.370

- Rs.380

- Rs.360

Solution 5.

Let us assume the cost of the watch on which profit was made is $x$. So the cost of the other watch is $(840-x)$.

The profit $=0.16x$, and

the loss $=0.12(840-x)$.

As there is no net loss or gain these two must be equal,

$0.12(840-x)=0.16x$,

Or, $4x=3(840-x)=3\times{840}-3x$,

Or, $7x=3\times{840}$,

Or, $x=3\times{120}=360$.

We have used the technique of equalizing the profit and loss amounts after choosing the variable $x$ judiciously along with delayed evaluation technique.

Answer: Option d: Rs.360.

Key concept used: Basic profit and loss concepts -- increment equalization technique, the profits and losses were the increments and decrements neutralizing each other -- delayed evaluation technique.

Problem 6.

A manufacturer sold an article to a wholesale dealer at a profit of 10%. The wholesale dealer sold it to a shopkeeper at 20% profit. The shopkeeper then sold it to a customer for Rs.56100 at a loss of 15%. The cost price of the article to the manufacturer was then,

- Rs.50000

- Rs.10000

- Rs.25000

- Rs.55000

Solution 6 - Problem analysis and solving

This is a problem of multistage transaction where at each stage the sale price of the previous stage becomes the cost price of the next stage. Profits or losses accordingly increases or decreases the amounts starting from the first cost price. Thus we won't calculate the profits, losses or amounts at each stage separately, doing it only once after establishing the relation between the first cost price and the last sale price.

Working backwards, the last sale price is,

$56100=0.85\text{ of last cost price}$, with 15% loss the sale price is less than the cost price by 0.15 times the cost price

Or, $56100=0.85\times{\text{shopkeeper cost price}}$

Thus,

$56100=0.85\times{\text{(shopkeeper cost price)}}$,

$=0.85\times{\text{(wholesale dealer sale price)}}$,

$=0.85\times{1.2}\times{\text{(wholesale dealer cost price)}}$, because of 20% profit by the wholesale dealer

$=0.85\times{1.2}\times{\text{(manufacturer sale price)}}$,

$=0.85\times{1.2}\times{1.1}\times{\text{(manufacturer cost price)}}$, because of the 10% profit by the manufacturer

So,

$\text{Manufacturer cost price }=\displaystyle\frac{56100}{0.85\times{1.2}\times{1.1}}$,

$=\displaystyle\frac{330000}{6.6}$, canceling factor 17 and multiplying 5 by 1.2

Or, $C=50000$.

Answer: Option a : Rs.50000.

Key concepts used: Basic profit and loss concepts -- multistage transactions -- percentage application for profit and loss -- efficient simpliffication -- working backwards approach.

Problem 7.

A house and a shop were sold for Rs.1 lakh each. The house sale resulted in a loss of 20% whereas the shop sale made a profit of 20%. The entire transaction then resulted in,

- No loss or gain

- Gain of Rs.$\frac{1}{24}$ lakh

- Loss of Rs.$\frac{1}{12}$ lakh

- Loss of Rs.$\frac{1}{18}$ lakh

Solution 7:

The sale price are same in two transactions as Rs. 1 lakh.

So in house transaction as the loss is 20%, the sale price of the house is, 80% of cost price, that is $\frac{4}{5}$th of the cost price. Thus,

Cost price of the house is, $\frac{5}{4}\times{\text{1 lakh}}$.

Similarly in the shop transaction as the profit is 20%, the sale price of the shop is, 120% of cost price, that is, $\frac{6}{5}\times{\text{Cost of shop}}$,

Or, $\text{Cost of the shop}=\frac{5}{6}\times{\text{1 lakh}}$.

Together, the total cost of the house and the shop is then,

$\left(\frac{5}{4}+\frac{5}{6}\right)=\frac{25}{12}=2\frac{1}{12}\text{of 1 lakh}$.

As this is more than the total sale price of 2 lakh, there is net loss of $\frac{1}{12}$ of Rs. 1 lakh, that is, loss of Rs. $\frac{1}{12}$ lakh.

Answer: c: loss of Rs. $\frac{1}{12}$ lakh.

Key concepts used: Basic profit and loss concepts -- percentage application for profit and loss -- efficient simplification, we have kept Rs. 1 lakh as a factor throughout knowing that it will be eliminated in the end; we did only fraction arithmetic -- delayed evaluation technique -- fraction arithmetic.

Problem 8.

A fruit seller sells lemons at the rate of 5 for 3 rupees which he bought at 2 for a rupee. His profit percent is,

- 10%

- 15%

- 25%

- 20%

Solution 8 - Problem analysis

If we find out per piece cost and sale prices we can find the profit or loss percent.

Solution 8 - Problem solving execution

The fruit seller buys 2 lemons for 1 rupee.

So per piece lemon cost is,

$\frac{1}{2}$ rupee.

Then he sells 5 lemons for 3 rupees.

So his per piece sale price is,

$\frac{3}{5}$ rupee which is more than the cost price.

So the profit on each $\frac{1}{2}$ rupee is,

$\frac{3}{5}-\frac{1}{2}=\frac{1}{10}$ rupee.

Profit percent is then,

$\frac{2}{10}=\frac{1}{5}=20\text{%}$, reverse conversion of profit as a fraction to profit as a percentage multiplying the fraction by 100.

Answer: Option d: 20%.

Key concepts used: Basic profit loss concepts -- base equalization, calculating the cost and sale prices per piece of lemon -- fraction to percent conversion -- unitary method.

Problem 9.

The ratio at which tea costing Rs.150/kg is to be mixed with tea costing Rs.192/kg so that the mixed tea when sold for Rs.194.40/kg gives a profit of 20% is,

- 2:5

- 3:5

- 5:3

- 5:2

Solution 9 - Problem analysis and solving

Let us assume in 1 kg of mixed tea we have mixed $x$ kg of tea costing 150/kg and so $1-x$ kg of tea costing Rs.192/kg.

Thus the total cost for each kg of tea becomes,

$C=150x +(1-x)192$.

By selling this 1 kg mixed tea at the price of Rs.192.40 a profit of 20% is made.

So,

$194.40=1.2C$,

Or, $C=\frac{194.40}{1.2}=162=150x +(1-x)192$,

Or, $42x=30$,

Or, $x=\frac{5}{7}$, that is, 5 portions of the 7 whole portions.

So the desired ratio is, $5:2$.

Answer: Option d: $5:2$.

Key concepts used: Basic profit and loss concepts -- mixing concept -- portions concepts, at the start itself only one variable in the mixture is assumed the other being in terms of the whole and the assumed variable $x$; this will ultimately result in ratio of variable to whole; subtracting variable portion from whole portion we will get the second mixed portion -- basic ratio concepts -- linear algebraic equations -- percentage application concept.

Problem 10.

The percentage loss when an article is sold at Rs.50 is the same as the percentage profit when it is sold for Rs.70. The loss or gain is,

- $20\text{%}$

- $16\frac{2}{3}\text{%}$

- $10\text{%}$

- $22\frac{2}{3}\text{%}$

Solution 10.

Cost prices in both situations is same and let us assume it to be $C$.

So, $(1-PL)C=50$, and

$(1+PL)C=70$, where loss and profit percentage is $PL$.

Taking the ratio and simplifying,

$5(1+PL)=7(1-PL)$,

Or, $12PL=2$.

Or, $PL=\frac{2}{12}=\frac{100}{6}\text{%}=16\frac{2}{3}\text{%}$

Answer: b: $16\frac{2}{3}\text{%}$.

Key concepts used: Percentage application for profit and loss -- assuming one variable for the same cost, two linear equations in two variables formed -- solving of two linear equations -- fraction to percent conversion.

Resources that should be useful for you

7 steps for sure success in SSC CGL tier 1 and tier 2 competitive tests or section on SSC CGL to access all the valuable student resources that we have created specifically for SSC CGL, but generally for any hard MCQ test.

Other related question set and solution set on SSC CGL Profit, loss and discount and Ratio and Proportion

SSC CGL Tier II level Solution Set 21 on Profit loss discount 4

SSC CGL Tier II level Question Set 21 on Profit loss discount 4

SSC CGL Tier II level Solution Set 20 on Profit loss discount 3

SSC CGL Tier II level Question Set 20 on Profit loss discount 3

SSC CGL Tier II level Solution Set 19 on Profit and loss 2

SSC CGL Tier II level Question Set 19 on Profit and loss 2

SSC CGL Tier II level Solution Set 8 on Profit and loss 1

SSC CGL Tier II level Question Set 8 on Profit and loss 1

SSC CGL level Solution Set 53 on Profit and loss 4

SSC CGL level Question Set 53 on Profit and loss 4

SSC CGL level Solution Set 34 on Profit and loss 3

SSC CGL level Question Set 34 on Profit and loss 3

SSC CGL level Solution Set 29 on Profit and loss 2

SSC CGL level Question Set 29 on Profit and loss 2

SSC CGL level Solution Set 25 on Arithmetic Percentage Ratios

SSC CGL level Question Set 25 on Arithmetic Percentage Ratios

SSC CGL level Solution Set 24 on Arithmetic Ratios

SSC CGL level Question Set 24 on Arithmetic Ratios

SSC CGL level Solution Set 6 on Profit and loss

SSC CGL level Question Set 6 on Profit and loss

SSC CGL level Solution Set 5 on Arithmetic Ratios

SSC CGL level Question Set 5 on Arithmetic Ratios

SSC CGL level Solution Set 4 on Arithmetic Ratios

SSC CGL level Question Set 4 on Arithmetic Ratios

How to solve difficult SSC CGL Math problems at very high speed using efficient problem solving strategies and techniques

These resources should be extremely useful for you to speed up your in-the-exam-hall SSC CGL math problem solving. You will find these under the subsection Efficient Math Problem Solving.

This is a collection of high power strategies and techniques for solving apparently tricky looking problems in various topic areas usually within a minute. These are no bag of tricks but are based on concepts and strategies that are not to be memorized but to be understood and applied with ease along with permanent skillset improvement.

The following are the associated links,

How to solve SSC CGL level Profit and loss problems by Change analysis in a few steps 6

How to solve a difficult SSC CGL level Profit and Loss problem in a few steps 4

How to solve difficult SSC CGL Profit and loss problems in a few steps 3

How to solve similar problems in a few seconds, Profit and loss problem 2, Domain modeling

How to solve in a few steps, Profit and loss problem 1